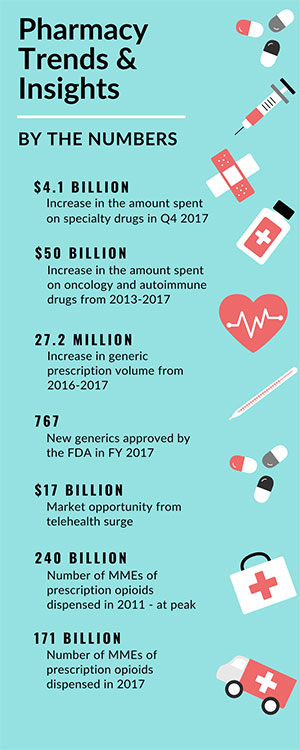

The year 2017 and early 2018 have been quite a whirlwind for the pharmacy industry. In terms of market performance, dollar growth remains in the low, single digits, following the Hepatitis C bubble in 2014 and 2015. Unadjusted script growth is flat year-to-date, while adjusted 90-day script growth is closer to ~2%. Ninety-day scripts are expected to continue at low, single-digit growth year over year, as higher adherence in Medicare Part D is pushed through the retail channel. It was also a major flu season, with almost 5 million affected per week during peak illness versus the peak of roughly 2.5 million weekly patients affected last season (2016-2017). Specialty growth rates continue to outpace traditional growth in 2017. Specialty spend increased $4.1 billion in Q4 2017 compared to a decline of $1.2 billion in traditional spend. Oncology and autoimmune are driving specialty growth and contributed to a combined ~$50 billion in absolute value growth from 2013 to 2017. Alternatively, Hepatitis C exhibited negative value growth of over $4 billion between 2016 and 2017. The decline in traditional spend can be partly attributed to loss of exclusivity, a decline in the pain class, and generic price deflation.

Regarding generics, 2017 was a record year for generic prescriptions in the US. Generic prescriptions reached an all-time high share of 85% of total market volume. From 2016 to 2017, generic volume went up 27.2 million scripts (+0.7%). This growth was primarily driven by chronic therapy areas, namely antihypertensives, mental health, lipid regulators, and diabetes. Last year was also a record year for generic approvals. The FDA approved 767 Abbreviated New Drug Applications (ANDAs) in fiscal year 2017. Generic drug applications are termed “abbreviated” because most do not require clinical trial data to establish safety and effectiveness. Instead, generic applicants must scientifically demonstrate bioequivalence as the innovative product. Of the 767 approvals in 2017, ~10% were unique molecule first-time approvals. This suggests new approvals may be joining markets partly saturated with manufacturers producing generics (or capable of producing the generic equivalent).

Generic price deflation and increased concentrated generic buying power contributed to a tough year for generic dollar share. Generic dollar share at 13.1% in 2017 is lower than it was in 2011. As of April 2018, generic dollar sales declined for 21 consecutive months, and 16 of the top 20 generic corporations (based on total generic sales) had negative dollar growth over the latest 12 months. To top it off, generic price deflation has yet to rebound in Q1 2018 and remained at -7.5% as of March 2018.

There has also been a lot of buzz around mergers/alliances, most notably regarding vertical integration. Amazon and Whole Foods, CVS and Aetna, and Cigna and Express Scripts are flipping the scripts for “traditional” corporate infrastructure. Much of the vertical integration can be attributed to organizations defending against Amazon. The CVS/Aetna and Cigna/Express Scripts mergers will undoubtedly maximize negotiating ability. It remains to be seen if Amazon will enter the market as a retail contender, but if there is any movement in pharmacy, the most logical point of entry is expected to be cash-paying patients for low-cost generics.

In terms of Market Access and Reimbursement, there have been six key issues that Market Access teams are facing. First, there has been tighter, more consolidated payer management, leading to more formulary drug exclusions and negotiations between PBMs and payers. Second, patients are facing higher out-of-pocket payments. In fact, the average commercial co-pay increased 14% between 2016 and 2017. Payers are also shifting more of the cost onto patients, although the majority of dispensed scripts (~80%) out-of-pocket cost is less than $10. Third, there has been amplified public pressure and demand for price transparency. State laws were passed to limit list price increases, and a handful of manufacturers (Abbvie, Allergan, etc.) publicly announced there will not be list price increases over 10%. This is supported by the March 2018 Price Auditor that finds brand inflation for the total market at 7.2%. Fourth, there are more stringent medical benefit management and increased medical benefit management techniques as specialty drugs have become increasingly costly. The vertical integrations across the industry aid in benefit management by allowing an increased ability to manage both pharmacy and medical costs. Fifth, value frameworks are expanding influence, and the use of value-based payment models and innovative agreements is increasing. In some cases, the scope of real-world evidence and outcomes-based measures now include “pay for performance.” This trend will likely continue in payment models going forward. Finally, the provider landscape is constantly evolving, with continued growth in the number of Integrated Delivery Networks (IDNs) and Accountable Care Organizations (ACOs). Some IDNs and ACOs have even evolved to influence prescribing decisions and manage drug utilization at the class level.

Opioids has been another hot topic amongst policy and regulation. Prescription opioid volume peaked in 2011 at 240 billion milligrams of morphine equivalents (MMEs) and has since declined by 29% to 171 billion MMEs in 2017. The number of retail opioid prescriptions declined 10.2% from January 2016 to December 2017. Extension of prescription drug monitoring programs, rescheduling of hydrocodone, and various state restrictions (i.e., 7-day limit) to opioid prescribing have attributed to the decline in opioid script volume.

Looking forward in 2018, “retailization of healthcare” is expected to grow. Retail-based health clinics present an opportunity for lower costs and more convenient settings for accessing healthcare. Retail pharmacies are also partnering with lab testing for diagnostic services. For example, Quest Diagnostics announced collaborations with Walmart and Safeway, and there are additional collaborations between LabCorp and Walgreens. Telehealth usage is expected to surge and Barclays estimates a potential addressable US market opportunity of $17 billion. Oncology will also continue to be a “high spend” therapy area, with about a quarter of new launches in 2017 attributed to the class and a robust R&D pipeline for supportive care/next generation biotherapeutics. It remains to be seen what impact biosimilars will have on the industry. To date, only 3 of 10 FDA-approved biosimilars have launched in the US. As pricing and reimbursement evolves, the uptake of biosimilars is expected to ultimately aid in cost savings.

IQVIA is an industry leader in Human Data Science. The ability to quantify the total market and provide insight on the pharmaceutical industry is unparalleled. To access IQVIA’s latest market reports and learn more about core capabilities, visit www.iqvia.com/institute/reports.

Disclaimer: The analyses, their interpretation, and related information contained herein are made and provided subject to the assumptions, methodologies, caveats, and variables described in this report and are based on third-party sources and data reasonably believed to be reliable. No warranty is made as to the completeness or accuracy of such third-party sources or data. As with any attempt to estimate future events, the forecasts, projections, conclusions, and other information included herein are subject to certain risks and uncertainties and are not to be considered guarantees of any particular outcome.

Comments (0)